Discover how to simplify your tax life by registering for CRA MyAccount with our step-by-step...

If the Canada Revenue Agency (CRA) has charged interest or penalties on your account, you may be able to request relief under the Taxpayer Relief Provisions. This applies to both individual (T1) and business accounts (T2, GST/HST, payroll, etc.).

This guide explains:

- How to identify interest and penalties

- Who qualifies

- Step-by-step how to apply (latest CRA process)

- What to include to improve approval chances

.jpg?width=1680&height=945&name=Toronto%20Trillium%20(3).jpg)

1. What Is CRA Interest and Penalty Relief?

The CRA has discretion to cancel or waive interest and penalties when taxpayers could not meet obligations due to circumstances beyond their control.

Important:

- Relief applies to interest and penalties only (not the tax owing)

- Requests must be within the last 10 years

- Each request is reviewed case-by-case

2. How to See Interest and Penalties (Personal & Business)

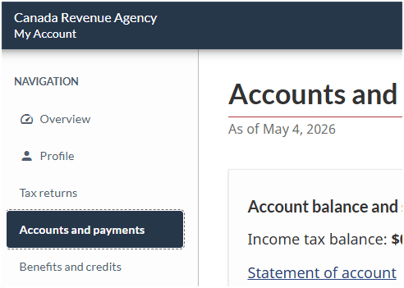

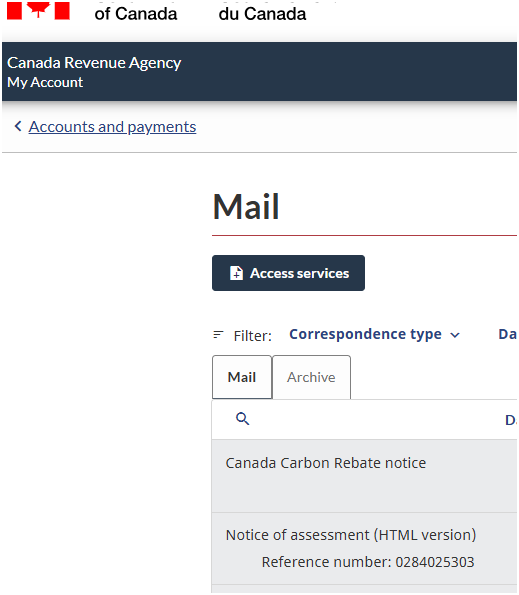

A. Personal (T1) – CRA My Account

- Log in to CRA My Account

- Go to:

- “Accounts and payments”

- “View mail” or “Statements of account”

- “Accounts and payments”

- Look for:

- Arrears interest

- Late-filing penalty

- Instalment interest/penalties

You can also review:

- Notice of Assessment (NOA)

- Reassessment letters

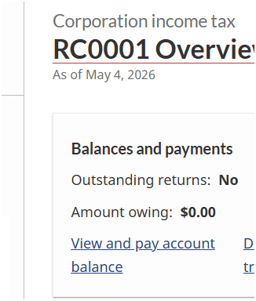

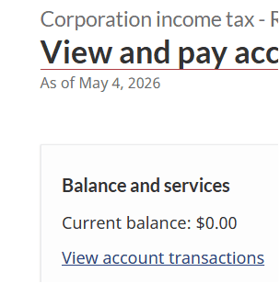

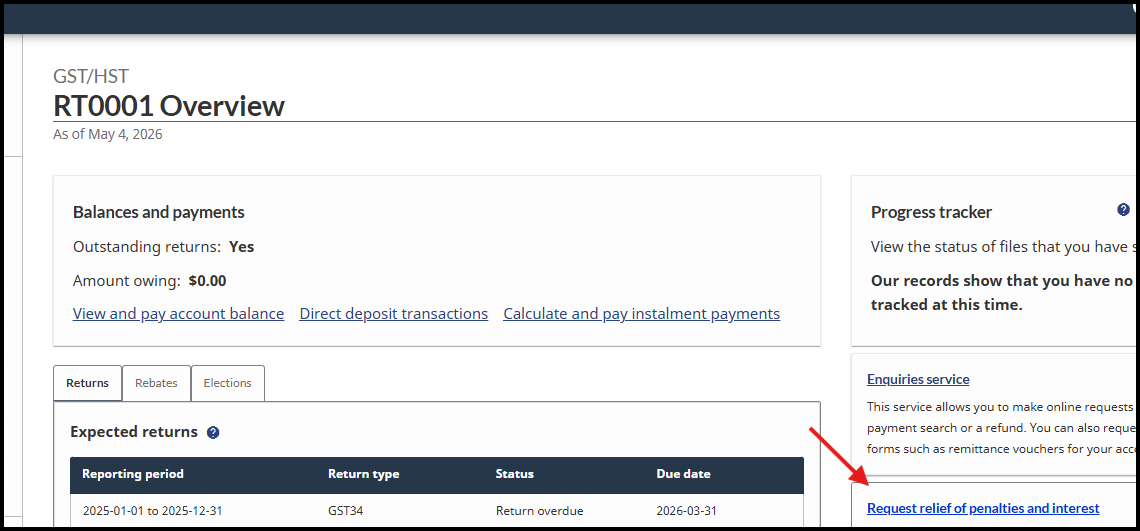

B. Business Accounts – CRA My Business Account

- Log in to CRA My Business Account

- Select the program account:

- RC (corporate tax)

- RT (GST/HST)

- RP (payroll)

- Go to:

- “View and pay account balance”

- “View transactions”

- “View and pay account balance”

You’ll see:

- Interest charged daily

- Penalty assessments

- Running balance

📌 Key point:

CRA interest is compounded daily and applied to unpaid balances and penalties.

3. When Can You Qualify for Relief?

Common accepted reasons:

1. Extraordinary circumstances

- Serious illness or accident

- Death in the family

- Natural disasters

2. CRA errors or delays

- Incorrect advice

- Processing delays

3. Financial hardship

- Unable to pay basic living expenses

4. Other exceptional situations

- Postal disruptions

- Unavoidable delays

You must clearly show how the situation prevented compliance (filing or payment).

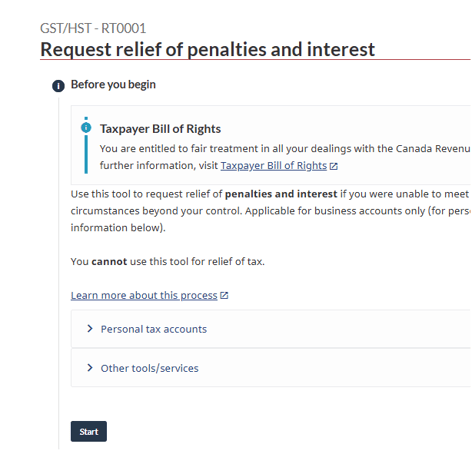

4. Step-by-Step: How to Apply

Option 1 (Recommended): Online via CRA Portal

You or your representative can submit directly through:

- CRA My Account (individual)

- CRA My Business Account (business)

- Represent a Client

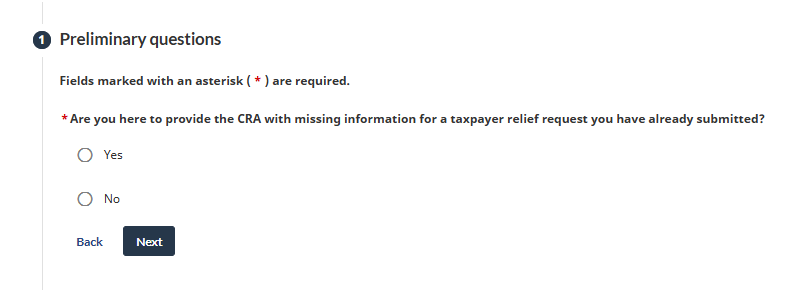

Steps:

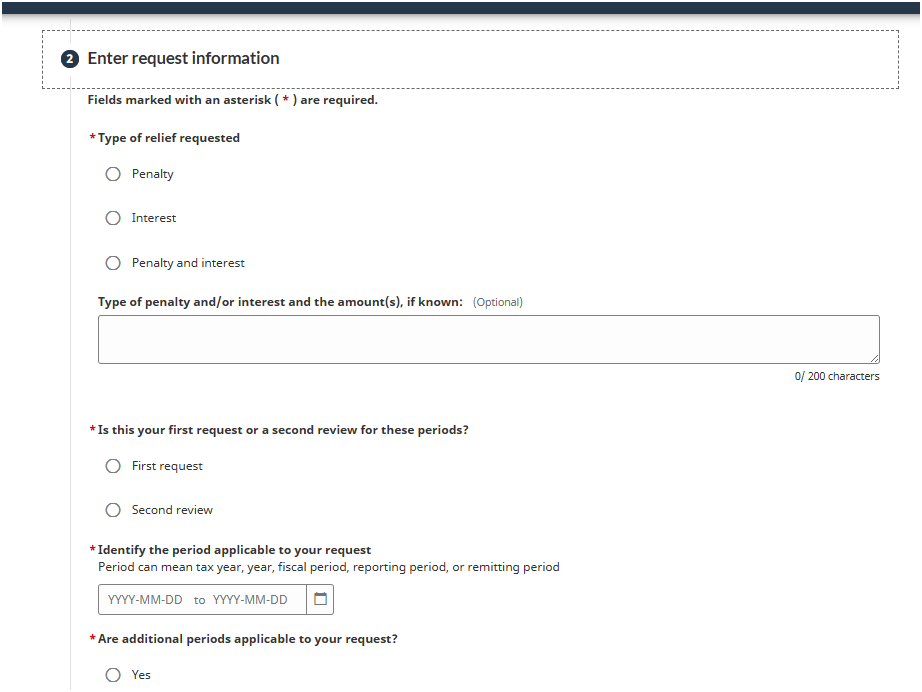

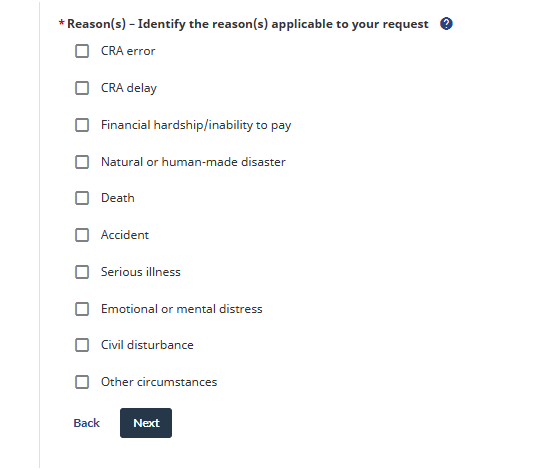

- Go to “Request relief of penalties and interest”

- Start to complete the form

- Answer the preliminary questions:

- Enter request information:

- Complete the request form with the information and options that best describes the situation.

- Upload supporting documents

This is the fastest method.

Option 2: Submit Form RC4288

Use:

- RC4288 Taxpayer Relief Request: RC4288 Taxpayer Relief Request - Cancel or Waive Penalties and Interest - Canada.ca

Steps:

- Complete the form

- Attach supporting documents

- Submit:

- Online via CRA “Submit Documents”, or

- Mail to CRA intake center

5. What to Include in Your Request

Your submission must be clear, detailed, and supported.

Required information:

- SIN or Business Number

- Tax year(s) or reporting period(s)

- Description of events

Supporting documents (examples):

- Medical records

- Death certificate

- Insurance claims

- CRA correspondence

- Financial statements (for hardship cases)

- Bank statements (last 3 months)

CRA expects full disclosure of your situation.

6. Best Practices to Improve Approval

From experience, approvals depend heavily on how the request is written:

Do:

- Clearly connect the event → inability to comply

- Use timelines (dates matter)

- Include proof for every claim

- Be concise but complete

Avoid:

- Saying “I forgot” or “I was busy”

- Submitting without documentation

- Requesting relief for very old periods (>10 years)

7. What Happens After You Apply?

- CRA reviews your request

- Processing time varies (often several months)

- If approved:

- Interest/penalties are reduced or removed

- If denied:

- You can request a second review

8. Key Limitations to Know

- CRA cannot cancel the tax itself

- Not all penalties qualify

- Relief is limited to the 10-year window

- Financial hardship alone is not always enough

9. Practical Example

Scenario:

A client files late due to hospitalization.

Strong request includes:

- Hospital admission/discharge dates

- Explanation of inability to manage finances

- Timeline showing missed deadline

- Supporting medical documents

Result: High chance of partial or full relief.

Final Thoughts

CRA interest and penalty relief is discretionary, but when done correctly, it can significantly reduce a client’s balance.

The key is:

👉 Strong documentation

👉 Clear explanation

👉 Proper submission through CRA portals

.png?height=200&name=Black%20White%20and%20Red%20Sleek%20Minimalist%20Photography%20Portfolio%20Presentation%20(1).png)